Abaxx Technologies: Filings Review 4/2/24

A review of financial filings and company progress.

Abaxx Technologies (ABXX) released its annual financials, AIF, MD&A, and the CEO has clarified some confusion on X. Let’s review.

Financial State

As noted in my last post on Abaxx, the company needed to raise money because it was at/close to running out of working capital (not dedicated to regulatory requirements).

Approximately $18M USD is required to uphold compliance with RMO and ACH licensing, so Abaxx was nearly running on empty. The start of exchange trading looked shaky without more financing.

Given the company has now raised $12M USD, with a burn rate of $4M USD per quarter, this gives Abaxx an additional three months of cash to fund operations through launch. They should have a cash position of around $31-32M USD.

Chances are, Abaxx will have to raise again in 2-3 quarters as ramping up open interest on an exchange isn’t a fast process. This is especially true when they’re eyeing an increase in R&D spend on the tech side to further build out ID++. The hope is that the company will be at a higher valuation by the time it needs to come back to market.

The estimated cash burn associated with technological R&D in 2024 seems to be around $4M USD:

The estimated cost to achieve commercial production for all applications is US$8 million. The net proceeds under the 2024 Bought Deal Offering are expected to fund approximately 40-50% of the necessary work to achieve commercial production. An additional amount of approximately US$4 million of expenditures is anticipated to be required to reach full commercial production across the five apps, with a projected development timeline of 12 to 18 months.

The company has around 540,000 options expiring throughout the rest of the year. Assuming they’re all exercised, the net proceeds would be around $4.4M USD. This could help fund operations for an additional quarter.

Additional Sources of Funding

As of December 31st, 2023, investments in Smart Crowd, Privacy Code, Pasig & Hudson, and AirCarbon totaled around $1.8M USD in value. These holdings remain unchanged.

Additional assets that could be monetized at some point, if necessary, are Abaxx’s 16% stake in Base Carbon and the LabMag/KeMag iron ore properties. The iron projects are currently valued at $0 (they were previously valued at around $1B at their peak in the last iron ore bull market).

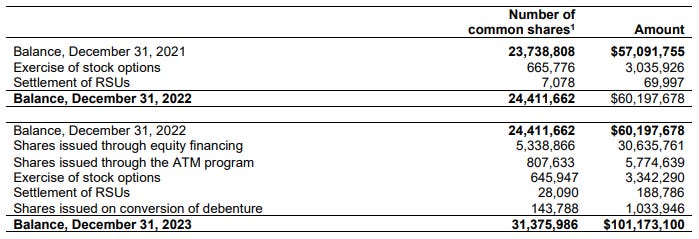

Share Capital

As of December 31st, 2023, Abaxx had approximately 31.4M shares outstanding. Add the 1.625M shares from the recent bought deal financing, and we’re currently sitting around 33M shares outstanding.

Company Progress

While Abaxx is clearly making progress, the “launch” of the exchange is seemingly delayed into Q2. I am hesitant to call it a delay— these expectations are really a result of poor communication about the trading process.

According to Josh Crumb, the CEO of Abaxx, all major market opening milestones are completed:

The third and final FCM necessary for launch was onboarded.

Abaxx’s BOD gave their attestations stating that they were ready.

Coordination of first market trades has begun.

Assuming this is all true, then we’re already “launched.” We just technically aren’t because the first trades haven’t been finalized yet.

The company intends to open the markets with “big players” contributing large physically-settled trades. Additional complexity associated with compiling these trades, back office negotiations, exchange preparations, etc has led to some spillage into Q2.

Abaxx is planning a call in mid-May to give themselves some time to build up open interest on the exchange and work out the starting block trades. This is combined with finishing a roadmap for their initial launch of ID++ in the public domain.

Can we really call things delayed if the first trades are already in progress? I suppose that’s in the eyes of the beholder.

As long as we’re moving along, I guess I can’t really complain. Although, it can certainly be annoying to think about how long things have dragged on.

There’s clearly a vast and complex nature to setting up an exchange of this scale. So we either continue to trust management and allow them to take their time and do things correctly, or we invest elsewhere.

I personally have no intention of selling out of the company for the foreseeable future. It turns out that this meme still applies:

Disclaimer: I’m long Abaxx Technologies. I hold an equity position that was acquired at an average share price of $5.51. I was not compensated by the company to create this post.

The owner of Green Investing is not a licensed investment professional. Nothing produced under the Green Investing brand should be construed as investment advice. My content is made for entertainment and educational purposes. Do your own research.

"The LabMag/KeMag iron ore properties" - how to even value this? Does that contrubute to revenues at least somehow?