Green Markets - March 29, 2025

News in environmental markets.

Green Markets is a weekly series dedicated to highlighting events of interest that could impact investments within environmental markets.

General Environmental/Regulatory

The SEC has announced it will no longer defend its climate disclosure rules in court, effectively halting enforcement and leaving the rule’s future in limbo. The rules, introduced in March 2024 to require public companies to report climate risks and emissions, had faced multiple legal challenges. Without SEC backing, courts could now strike down the rule without the agency formally rescinding it.

Republicans are considering a “thoughtful” phaseout of clean energy tax credits from the Inflation Reduction Act (IRA), rather than a full repeal. House Budget Chair Jodey Arrington (R-Texas), once a vocal critic of the credits, now suggests a gradual transition to avoid disrupting markets. The shift comes amid internal GOP tensions, as nearly two dozen Republicans have expressed support for preserving the credits due to local economic benefits. With limited climate funding to cut, Republicans are reassessing their approach as they work to offset the cost of extending the 2017 Trump-era tax cuts in the upcoming reconciliation bill.

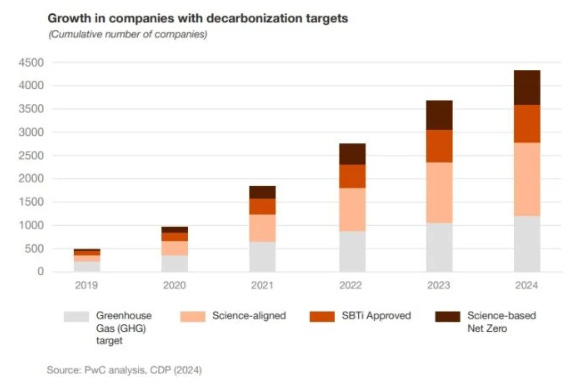

A new PwC report reveals that 84% of companies are maintaining or accelerating their climate commitments, despite economic uncertainty and evolving regulations. Sustainability efforts are delivering financial benefits, with eco-friendly products earning 6% to 25% more than conventional ones, and smaller businesses are increasingly joining the decarbonization movement due to supply chain pressures.

Battery Metals

J.P. Morgan has upgraded the mining and metals sector to “overweight,” citing a projected rebound in commodity prices and improving fundamentals, especially in copper. The firm expects a V-shaped recovery driven by China’s recent economic stimulus measures and tightening supply-demand dynamics, with copper forecast to rise 15% to $11,500/ton by Q2 2026. Mining equities have significantly underperformed since 2023, creating a valuation gap that J.P. Morgan sees as a strong upside opportunity.

Rebels from Myanmar’s Kachin Independence Army (KIA) have seized control of rare earth mines producing about half of the world’s heavy rare earths, significantly disrupting supply chains and driving up prices, especially for terbium oxide. The KIA is using these resources to pressure China, which supports Myanmar’s military junta and relies on these mines for critical minerals used in EVs and wind turbines. India has shown interest in stepping in but faces logistical and processing challenges.

There are conflicting reports, Reuters states that the rebel group will allow the exportation of rare earths minerals to China.

Tin prices surged after an earthquake in Myanmar raised concerns about delays in restarting mining operations in Wa State, which produces 70% of the country’s tin. Although the quake’s epicenter was over 400 km from the mining region, speculators drove prices up 2.5% to $36,140 per metric ton. Myanmar is a major tin supplier to China, and ongoing production suspensions since August 2023 were already tightening global supply. Combined with a halt at Alphamin’s mine in the DRC and low LME inventories, the market remains highly sensitive to any disruptions.

Some of the battery metals like cobalt and lithium have had their prices experience precipitous declines after EV demand fell off. Firms like Goldman Sachs are starting to predict that lithium might have bottomed here or in the near future. See the chart below:

Biofuels/Chemicals

IATA has launched the Civil Aviation Decarbonisation Organisation (CADO) to operate its upcoming Sustainable Aviation Fuel (SAF) Registry, aiming to create a transparent, global system for tracking SAF use and claims. CADO will be an independent body that is open to all SAF value chain stakeholders.

Carbon Capture

Shell, Equinor, and TotalEnergies will invest $714 million to expand their Northern Lights carbon storage project in Norway, following a 15-year deal with Stockholm Exergi to store 900,000 tonnes of CO2 annually. The expansion will more than triple the facility’s capacity to 5 million tonnes per year— roughly 10% of Norway’s annual emissions. The investment also includes €131 million in funding from the European Commission, signaling strong EU support for large-scale carbon capture and storage (CCS).

Compliance Carbon Markets (CCMs)

China will expand its national carbon trading market to include the steel, cement, and aluminum industries, adding around 1,500 new firms to the scheme. This move will increase the program’s coverage to 8 billion metric tons of CO2, over 60% of China’s total emissions. This makes it the world’s largest carbon market by volume.

Mexico is set to bring its emissions trading system (ETS) online by the end of the year. The system will include the usage of carbon offsets. Details are scarce because Carbon Pulse is paywalled for institutional clients only.

Voluntary Carbon Markets (VCMs)

The Science Based Targets initiative (SBTi) has released a draft update to its Corporate Net-Zero Standard (CNZS), firmly limiting the use of carbon credits for Scope 3 emissions, emphasizing instead internal decarbonization and action-based targets. The move follows internal dissent and external criticism over earlier proposals to expand carbon credit use. While carbon credits remain part of recommended “beyond-value chain mitigation” strategies, they can no longer be counted toward core abatement goals. The final publication of the standard is expected in 2026 following pilot testing and further consultation.

Liquified Natural Gas (LNG)

U.S. natural gas demand is projected to remain at record highs through 2026, fueled by booming LNG exports and rising electricity consumption from new data centers. The U.S. remains the world’s top gas producer, but a lack of pipeline infrastructure is creating bottlenecks, driving up electricity costs and limiting supply delivery. EQT and ONEOK emphasized that pipeline investment is lagging, with projects like the Mountain Valley Pipeline taking years and billions over budget to complete.

Btw, I read a report stating that lithium is not particularly rare, quite opposite. Will you agree?